Ok, I have been officially quarantined for one hundred and thirty-seven days. Am I suffering from claustrophobia? Have I, all of a sudden, started advocating against my deepest beliefs? Have I just finished teaching a class on motivating students into doing something that does not work? Am I working into further developing a practice that, in the end, will not succeed? Have I given up on ‘steering the Titanic’ into a different way of investing?

While I will admit that the lockdown is starting to look, well, a little bit ‘repetitive’, I am more convinced than ever than impact investing is here to stay and that it will continue to grow at a more rapid pace than ever before. Is then there a contradiction with the title of this article? I hope not. What I am seeking to convey is that it is not necessarily healthy when major investment funds, banks, consultancies, business lobby groups, and governments all recklessly jump into the impact bandwagon.

I have identified three main perils associated to the ‘bandwagon’ behavior: (i) neither understanding nor knowing what impact investment means and which impact investments actually do make sense and can qualify as such; (ii) ‘manufacturing’ extensive and massive impact stories for expectant investors; and, (iii) reporting impact ‘creation’ in a non-measurable way, with the goal of obscuring the fact that there’s simply no investment additionality.

Defining it to understand it

On (i), there is simply no way that you can magically ‘convert’ all investments into impact deals. In some industries and cases, it simply does not work. For instance, Alan Schwartz and Reuben Finighan have just published an article on HBR titled, Why Impact Investing Won’t Save Capitalism. The article is well written and has some very valid points – but its title is, in my opinion, somewhat misleading. Impact investing has not been designed to ‘save’ anything – let’s try to demystify that.

It is simply a form of investing under which certain types of projects, where profitability and a socio-economic return might simultaneously be achieved, can be pooled and funds can be raised to do more of these as the industry continues to grow. There is simply no way that you can fit all possible investments under the impact umbrella.

Like in a harvest of selected grapes to produce the finest wines, you need to cherry pick each grape until your farm is large enough to leverage on a larger critical mass.

The same authors argue that, “there are simply not enough below-the-line options to invest in, and much of what we must do will be unprofitable without a change in the rules”. In my opinion, that is not the immediate problem that we must tackle – the challenge is on investors to make the pie larger and discover those below-the-line options that are currently being ignored. Note: Schwartz and Finighan define as initiatives “below the zero-cost line as those profitable for impact investors without any change in current policies.”

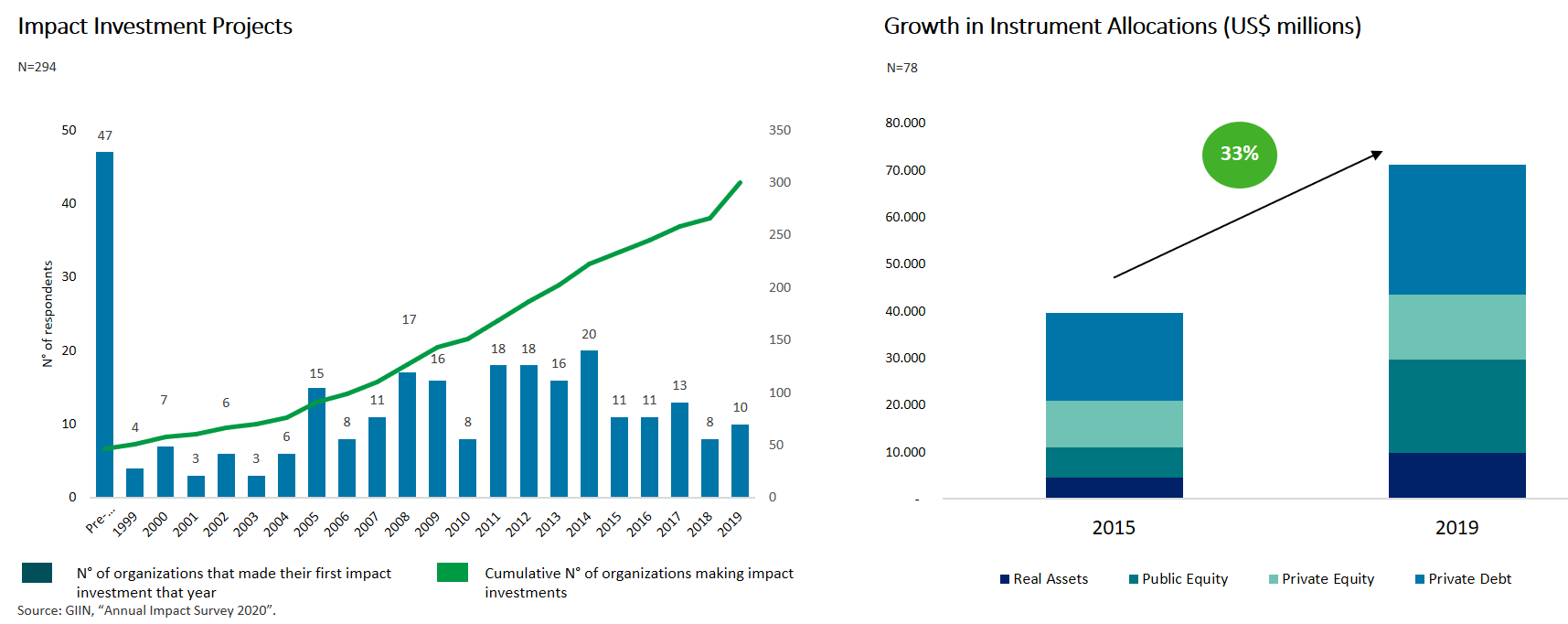

As the charts below from the GIIN’s 2020 survey shows, impact investors are indeed cherry picking more actively and increasing the size of the ‘impact farm’.

The gold pot at the end of the rainbow

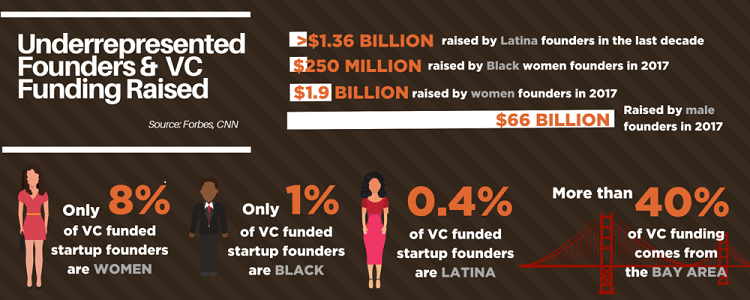

On (ii), Sir Ronald Cohen’s impact revolution is full of examples on how the shift into an impact mentality has been happening gradually. And, while I recognize ‘traditional’ investors for paying more attention to impact, in some cases the story just seems a bit forced and too opportunistic. Take, for instance, the case of SoftBank, a ‘mega’ fund that recently announced that it would invest $100 million in minority-owned businesses. Commendable for sure. However, the amount pledged is about 0.1% the amount of SoftBank’s much larger Vision Fund, which the company started deploying in 2017.

Compound this with the fact that the fund has invested in just one company with a sole founder who was black, and one other company with a black co-founder, over its three-year existence. SoftBank might have all the right intentions, but it needs to be put under scrutiny and, while $100 million was, when announced, the largest single pool of capital available for underrepresented founders, it needs to be held accountable and deliver.

Metaphorically, we all marvel when the sky gifts us with a rainbow after a storm, but it is much harder to find the gold pot at the end of the rainbow when it dissipates.

And SoftBank is not the only case – other large LBO-driven funds have recently argued that they have been doing impact investing for more than a decade. And that, suddenly, they have now realized that it was the right time to pool those impact investments into a fund and go raise extra capital from investors. Now, these fund managers are incredibly smart people, so forgive me for being a bit skeptical on them not having reaped the rewards of ‘doing well while making money’ and just letting a decade pass by.

Simplistically, a search for “new diversity funds in 2020” on Google for articles published over the last seven days will yield you thousands of results. Again, looking at the rainbow is nice, but finding the gold pot is much harder.

Impact measurement as a way to legitimize impact investing

On (iii), impact measurement and management includes identifying and considering the positive and negative effects one’s business actions have on people and the planet, and then figuring out ways to mitigate the negative and maximize the positive in alignment with one’s goals. There are many reasons why impact measurement and management (IMM) has become more critical than ever before. I have chosen to highlight the following three:

Reason #1: across a portfolio, impact measurement facilitates learning, enabling investment decisions to be better tuned towards achieving impact. Companies that are able to demonstrate that their business has a broader impact may also be more successful in attracting further investment capital.

Reason #2: the conversation around impact measurement has evolved in recent years from ‘accountability’ to ‘standards’ and now to ‘value’: while accountability and standards – which help facilitate the comparison of different types of impact – are vital to impact measurement, investors need to gather this data, analyze it, learn from it and use that knowledge to improve upon impact practices.

Reason #3: one of the greatest risks of mobilizing capital to the impact sector is the potential for impact washing. Impact investors need to be looking behind the curtain on investments to maintain credibility. As highlighted earlier in this article, and in other pieces that I have written on this topic, there are examples of investments and funds being marketed as impact investments without the impact management practices in place to substantiate this label.

A few weeks ago, I was offered to invest in an impact-oriented fund that had year-to-date returns much higher than those of its peers. I asked the fund manager if they could give me an example of an impact investment that they had recently made. “Well, we just bought several shares of Gilead Sciences“, they wrote back. You may know that Gilead Sciences, is a large pharmaceutical company (latest market cap of $87 billion) that develops and produces drugs for severe diseases, such as HIV, and it is leading one of the efforts to find a vaccine against Covid-19.

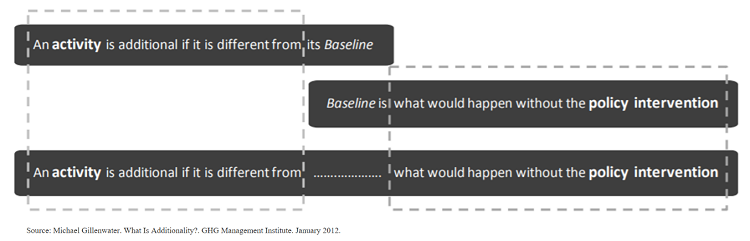

I then asked what percentage of shares of Gilead Sciences the fund did own and how they reported impact. The answer I got was, “Well, it is a large company, but we bought like $1 million and we are reporting the number of HIV patients treated with the drugs produced by Gilead – great story!”. That is, I am afraid, not impact. The question to answer is: if I invest in the fund, do more HIV-positive patients receive treatment? Unlikely in a company of this size, unless I make a really big investment and can encourage any change in the company – a concept defined by impact investors as ‘additionality’.

Would you rather read about a more ‘objective’ example? Well, you have to look no further than this week’s Financial Times article on the recent collapse in the shares of Boohoo, a British fast fashion retailer. Boohoo was accused of underpaying workers in its UK supply chain and declining to publish a list of its suppliers. Yet, Boohoo was one of the ‘darlings’ of the ESG ratings agencies, receiving a score of 8.4 out of 10 from MSCI, well above the industry of 5.5. Furthermore, twenty ‘sustainable’ funds had put money into Boohoo, including funds that invest in companies with ‘good employment opportunities and practices’. As the article rightly states, it may be right that there can be no conflict between doing good and doing well, but it is also true that companies can make a lot of money “by compressing labor costs before policymakers and regulators catch on.”

The challenge: aligning companies with impact investors

Schwartz and Finighan argue that the most important role for impact investors is to lobby for changing the rules. Sure, as impact investors continue to evolve into a larger group, and the ‘big’ players come into the picture, their lobbying capacity will become more significant. No question about that. That does not translate into recklessly jumping into the impact bandwagon – it means growing the asset responsibly and credibly.

However, I personally believe the pie is still too small, and that impact investors currently have plenty of opportunities to continue to develop the industry at an ‘exponential rate’ – using Covid-related terms with a nicer twist. Perhaps, the most pressing challenge could be that both investors and companies need to find a better way to align themselves under a common impact investment thesis? As impact continues to become more relevant, regulation will continue to follow and, gradually, the case for a shift in the rules of the game will become easier to make. In the words of Alvin Toffler, “The illiterate of the 21st century will not be those who cannot read and write, but those who cannot learn, unlearn, and relearn.”